The global coffee market showed renewed momentum this week as coffee prices rebounded sharply across major international exchanges, raising expectations that Vietnam’s coffee export industry could regain growth momentum in the coming quarters. After months of price corrections and softer export revenues, the recovery in both Arabica and Robusta futures is providing cautious optimism for exporters, traders, and farmers throughout the supply chain.

The latest market rally comes amid growing concerns over global supply conditions, particularly in Vietnam and Brazil – the world’s two largest coffee-producing nations. Weather irregularities, slower harvest progress in Brazil, tightening certified inventories, and continued farmer stockholding behavior have all contributed to stronger bullish sentiment across coffee markets.

At the same time, Vietnam’s export industry is navigating a complex transition period. While export volumes continue to rise, lower average selling prices have weighed heavily on export revenues during the first months of 2026. Industry experts now believe that improving market conditions and stronger price recovery in May could help restore value growth during the second half of the year.

Global Coffee Futures Rally on Supply Concerns

Coffee prices recorded strong gains on both the London and New York exchanges during the latest trading sessions. On ICE Futures Europe in London, July 2026 Robusta contracts climbed above the critical threshold of $3,500 per ton, reflecting growing market anxiety over near-term supply availability. Arabica futures on ICE Futures US in New York also moved higher, supported by similar concerns surrounding premium coffee supply.

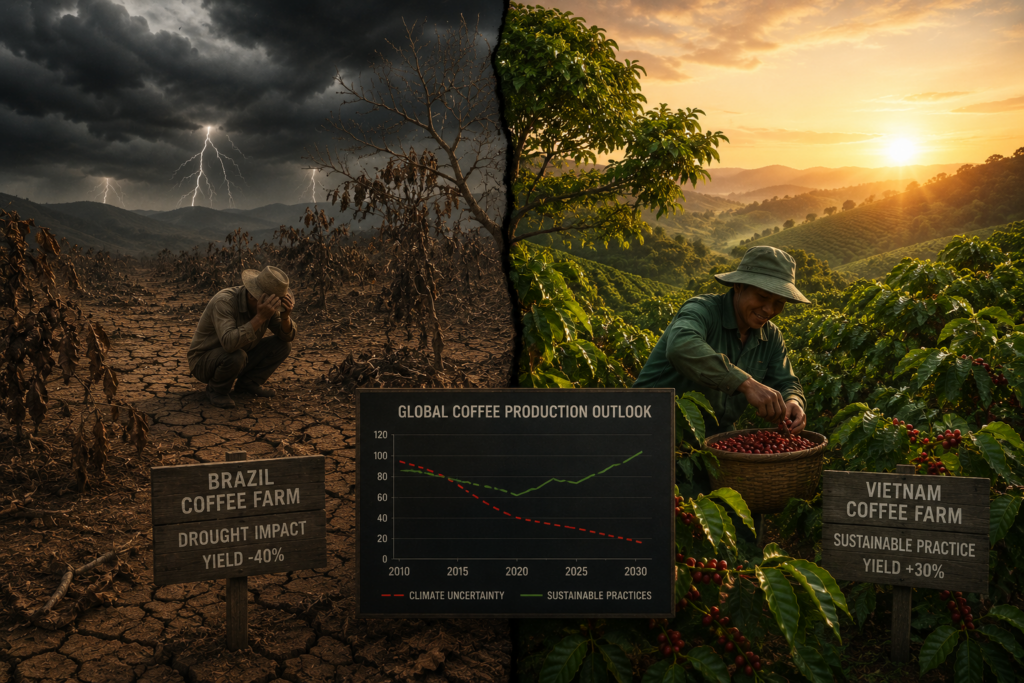

Market analysts attribute the recovery primarily to uncertainty surrounding production prospects in major exporting countries. In Vietnam, uneven rainfall distribution and localized drought conditions across the Central Highlands have raised concerns about the outlook for the 2026/27 crop season. Weather forecasters continue to monitor the potential impact of El Niño conditions, which could negatively affect yields and bean quality if dry conditions intensify later in the year.

The market has responded quickly to these risks. Speculative buying activity increased significantly on the London exchange, helping push Robusta prices upward after several weeks of weakness. Investors are closely watching Vietnam because the country remains the world’s largest supplier of Robusta coffee, which is increasingly important for global instant coffee manufacturers and commercial roasters.

Low certified coffee inventories on ICE exchanges have also provided additional support to prices. Stocks remain below historical averages, while many farmers in producing regions continue to limit sales in anticipation of further price increases. This slower pace of physical trading has created tighter short-term supply conditions in the international market.

Brazil’s Slow Harvest Adds Market Pressure

Brazil’s harvest season is progressing more slowly than expected, creating additional uncertainty for global supply chains. Although Brazil is still projected to produce a large crop this year, actual harvesting activity remains behind historical averages.

According to industry reports from Safras & Mercado and StoneX, Robusta harvest progress in Brazil had reached only around 13 -14% by late May, well below both last year’s pace and the five-year average. Arabica harvesting activity has also lagged behind previous seasons.

The delayed harvest has temporarily tightened export availability and supported market prices. Traders are increasingly concerned that logistical bottlenecks or weather disruptions during Brazil’s winter season could further slow supply flows to global markets. Frost risks remain a particularly important variable because severe cold weather in Brazil can dramatically alter global coffee price trends within days.

Despite these short-term concerns, broader supply expectations remain relatively positive. Forecasts from several international institutions continue to suggest that Brazil could deliver one of its stronger harvests in recent years if weather conditions remain favorable throughout the remainder of the season.

Vietnam’s Coffee Exports Face Price Pressure

Vietnam’s coffee export industry has experienced mixed results during the first four months of 2026. Export volumes continued to rise strongly, demonstrating resilient international demand for Vietnamese coffee, especially Robusta. However, falling global coffee prices earlier this year significantly reduced export revenues.

According to Vietnam Customs data, the country exported approximately 782,000 tons of coffee during the first four months of 2026, generating around $3.58 billion in export revenue. Export volumes increased by nearly 12% compared with the same period last year, but export value declined close to 10% due to lower average prices.

The decline in export value largely reflects the sharp correction in coffee prices after the historic rally seen throughout much of 2025. Average export prices during the first four months of 2026 fell to roughly $4,575 per ton, representing a year-on-year decrease of almost 20%.

This price correction was driven by expectations of improving global supply, particularly from Brazil, Vietnam, Uganda, and several other producing nations. Global production forecasts from StoneX suggest that coffee output in 2026 could exceed worldwide consumption by approximately 10 million bags, creating fears of a potential market surplus.

Even so, Vietnam has maintained strong positioning across its major export markets. The European Union remains the largest destination for Vietnamese coffee exports, with Germany, Italy, and Belgium continuing to show stable demand. Vietnamese Robusta remains highly competitive in Europe thanks to its price efficiency and increasing quality improvements.

China has also emerged as one of the fastest-growing markets for Vietnamese coffee. Rising coffee consumption among younger Chinese consumers and rapid café expansion across major cities are creating significant long-term opportunities for Vietnamese exporters. Export growth to China has increased sharply both in volume and value over the past year.

Meanwhile, the United States continues to maintain stable coffee import demand despite broader economic uncertainty. Although growth rates are more moderate compared with Asian markets, the U.S. remains one of the most important high-value destinations for global coffee exporters.

Industry Pushes Toward Higher Value Products

The recent volatility in coffee prices has reinforced the urgency for Vietnam’s coffee industry to move beyond raw bean exports and focus more heavily on value-added processing. Industry leaders increasingly view deep processing as essential for long-term growth and greater protection against commodity price fluctuations.

Vietnam has historically dominated the global Robusta segment through large-scale production, but experts argue that future competitiveness will depend more on quality differentiation, sustainability standards, and brand positioning rather than volume alone.

Programs such as the “Robusta XXI” initiative are being promoted to establish stronger quality standards for Vietnamese Robusta coffee. The initiative aims to create scientifically based quality evaluation systems capable of improving international recognition for Vietnamese coffee products.

At the same time, demand for sustainable and traceable coffee continues to rise in major importing markets. European buyers, in particular, are placing greater emphasis on environmental certifications, supply chain transparency, and sustainable farming practices. This trend is expected to accelerate following stricter sustainability regulations within the European Union.

As a result, Vietnamese exporters are increasingly investing in roasted coffee, instant coffee, specialty coffee, and certified sustainable products rather than relying exclusively on green bean exports. Many analysts believe this transition will be critical for improving export profitability over the next decade.

Outlook for the Second Half of 2026

The recovery in global coffee prices during May has improved sentiment across the industry, but uncertainty remains high. Weather developments in Vietnam and Brazil will continue to dominate market direction over the coming months, while harvest progress and global inventory levels remain closely monitored by traders.

If current price recovery trends continue, Vietnam’s coffee export sector could regain stronger value growth during the second and third quarters of 2026. However, analysts caution that long-term stability will depend less on short-term price rallies and more on the industry’s ability to strengthen quality, expand processing capacity, and adapt to changing consumer preferences worldwide.

For global coffee markets, the current environment reflects a delicate balance between improving supply prospects and persistent production risks. While stronger harvest expectations from Brazil and Vietnam may eventually place downward pressure on prices again, short-term concerns surrounding weather conditions and delayed harvest activity are likely to keep volatility elevated throughout the remainder of the year.

{kind=link}