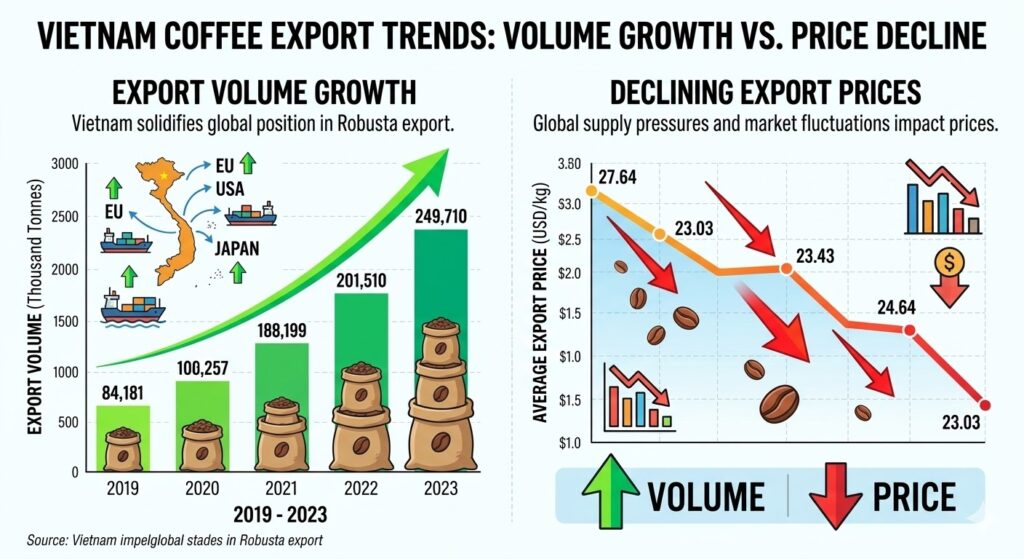

Vietnam’s coffee sector started 2026 with a paradox: export volumes surged, but export prices declined sharply. The development highlights the growing complexity of the global coffee market, where strong demand does not always translate into higher revenues for producing countries.

According to official customs statistics cited by VietnamBiz, Vietnam exported 367,270 tonnes of coffee in the first two months of 2026, representing a 14.5% increase compared with the same period in 2025. However, export revenue reached only $1.76 billion, down 1.3% year-on-year, reflecting a significant decline in international coffee prices.

The decline highlights the growing pressure on coffee-producing nations as global supply conditions improve and speculative momentum fades from commodity markets.

Export Prices See Sharp Decline

One of the most notable trends in the early months of 2026 is the rapid fall in Vietnam’s coffee export prices.

The average export price during January–February 2026 dropped to $4,779 per tonne, a 13.8% decline compared with the same period last year. In February alone, export prices averaged $4,718 per tonne, down 16.5% year-on-year and 2.1% lower than January.

This marks the lowest export price recorded since July 2024, signaling a clear shift in market dynamics after the record highs seen in 2024 and early 2025.

Several factors contributed to this decline:

- Improved supply outlook from major producers such as Brazil

- Profit-taking by speculative funds after the previous price rally

- A temporary slowdown in trading activities across the global coffee market

Reports from the global coffee market also indicate that price indices began trending lower as supply expectations improved and market sentiment cooled after the previous year’s tight supply conditions.

February Export Activity Slows

Vietnam’s coffee exports slowed significantly in February, partly due to seasonal factors.

During the month, exports totaled 142,337 tonnes worth $671.5 million, representing a 36.6% drop in volume and a 37.9% drop in value compared with January. On a year-on-year basis, export volume declined 19.8%, while export value fell 33%.

The sharp monthly drop was largely attributed to the Lunar New Year holiday, which reduced working days and temporarily disrupted procurement, processing, and logistics activities within the coffee supply chain.

However, market analysts emphasize that the February slowdown should not be interpreted as weakening demand. Instead, it reflects seasonal export patterns that typically occur during the Vietnamese holiday period.

Europe Remains Vietnam’s Largest Coffee Market

Despite declining prices, global demand for Vietnamese coffee remains strong, particularly in Europe.

The European Union continues to be Vietnam’s largest export destination, accounting for nearly 49% of total export volume and 46.8% of export value during the first two months of 2026. Vietnam exported 179,598 tonnes of coffee to the EU, generating $822.2 million in revenue.

Major European markets including Germany, Italy, and Spain recorded strong growth:

- Exports to Germany increased about 30%

- Shipments to Italy rose 8.8%

- Exports to Spain surged 44.3%

These figures underline Europe’s continued reliance on Vietnam as a critical supplier of robusta coffee for the continent’s large roasting industry.

Outside Europe, several emerging markets also showed impressive growth. Exports to Russia increased by 29.2%, while shipments to Algeria rose 46.8% and exports to China jumped 49.1%.

China’s growing coffee consumption remains a particularly important trend, as the country continues to develop a rapidly expanding specialty and café culture.

Domestic Coffee Prices Follow Global Downtrend

The decline in export prices has also been reflected in Vietnam’s domestic market.

As of mid-March 2026, farm-gate coffee prices in the Central Highlands ranged between 93,200 and 94,000 VND per kilogram, representing a decline of about 3–4% compared with the previous month.

More strikingly, domestic prices are now nearly 30% lower than the peak levels recorded in early 2025, when robusta prices surged amid severe global supply concerns.

International futures markets have also softened:

- London robusta futures for May 2026 recently traded around $3,625 per tonne

- New York arabica futures hovered near 291.9 US cents per pound

Both benchmarks have retreated significantly from last year’s highs as expectations of larger global harvests weigh on market sentiment.

Global Supply Outlook Pressures Coffee Prices

A major factor behind the weakening price environment is the improving supply outlook from key producing countries.

Brazil, the world’s largest coffee producer, is expected to harvest a strong crop this year after favorable rainfall improved crop conditions. Traders believe the prospect of a larger Brazilian harvest is putting significant downward pressure on international coffee prices.

At the same time, Vietnam’s own production outlook remains stable, with export volumes continuing to grow despite falling prices.

For global coffee buyers and roasters, the current market conditions offer opportunities to rebuild inventories after the tight supply environment of the previous year.

Outlook: A Market Transition Phase

Looking ahead, the global coffee market appears to be entering a transitional phase.

While consumption remains resilient in major markets such as Europe and Asia, the balance between supply and demand is gradually shifting. With higher production expected from Brazil and other producers, the market may move from a supply deficit toward a more balanced — or even surplus — environment.

For Vietnam, this means that export growth alone may not guarantee rising revenues. Instead, the industry will increasingly need to focus on:

- value-added processing

- specialty coffee production

- deeper market diversification

As global coffee prices fluctuate, Vietnam’s long-term competitiveness will depend on how effectively it moves up the value chain.

{kind=link}