The sudden escalation of hostilities between Israel and Iran in early March 2026 — marked by coordinated strikes on Iranian territory by U.S. and Israeli forces and forceful missile retaliation by Tehran — has reverberated far beyond the immediate war theatre. While coffee production does not originate in either nation, this conflict has triggered multi-layered impacts on global commodity markets, transportation networks, energy prices, risk sentiment and supply-chain dynamics that materially influence coffee markets worldwide.

Geopolitical Shock, Shipping, and Logistics

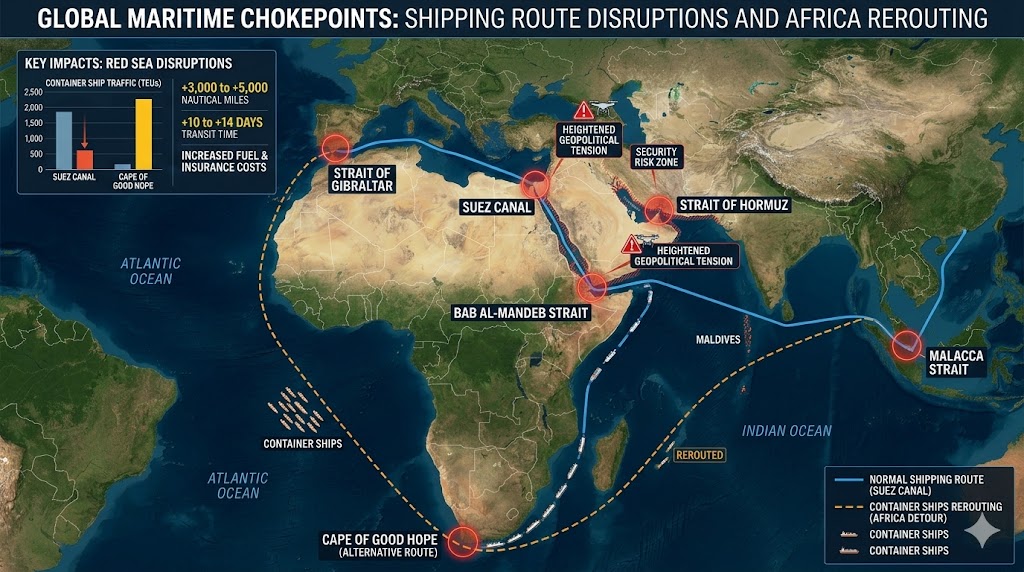

The most immediate mechanism through which the Iran–Israel standoff affects coffee is logistics and maritime risk. The Middle East, particularly the Persian Gulf and adjacent chokepoints such as the Strait of Hormuz and Suez Canal routes connecting to the Red Sea, sits at the nexus of global trade routes. Recent reports confirm fears that disruptions in this region — including threats to close hormone-critical transit lanes — have elevated risk levels for global shipping and tanker insurance, pushing freight rates sharply higher.

Coffee supply chains are especially sensitive to delays and cost increases in international freight. Although green coffee beans are not harvested in Iran or Israel, beans exported from East Africa and Latin America typically transit through Red Sea and Mediterranean corridors to reach European and North American roasters. Geopolitical instability in the Gulf often spills over into these interconnected networks. Prior episodes of Red Sea unrest — notably from Houthi attacks on commercial shipping — have led to major rerouting of cargo ships around Africa, adding 10–14 days or more to transit times and significantly increasing costs.

Even absent direct hostilities in coffee-producing regions, such extended delivery times ripples up the supply chain:

- Container availability tightens, as vessels are tied up longer on rerouted journeys;

- Storage and demurrage fees rise, pressuring exporters and importers alike;

- Lead times elongate, creating inventory uncertainty for roasters and traders who typically plan months ahead.

In short, shipping cost inflation and transit bottlenecks translate into higher landed costs for coffee, squeezing profit margins in an already tight commodity market.

Energy Prices, Input Costs, and Coffee Economics

A second transmission channel is energy cost inflation. The Middle East conflict immediately triggered a sharp spike in crude oil prices — with Brent crude climbing rapidly and analysts warning it could approach or exceed $100 per barrel if the crisis worsens.

Coffee supply chains are highly energy intensive:

- Fuel is a major component of transportation costs by truck, rail, and ocean freight;

- Electricity and diesel power coffee milling and processing in producer countries;

- Energy costs influence storage, refrigeration, and roasting operations globally.

When crude climbs quickly, logistics providers raise freight and fuel surcharges, which roasters typically pass down the supply chain or hedge through futures pricing. Energy cost increases also exert inflationary pressure on other input categories such as fertilizers, packaging and labor costs, compounding supply-side inflation for coffee producers. The net effect is often upward pressure on coffee prices for both futures and physical markets.

Financial Market Volatility and Risk Premiums

Beyond physical supply chains, the geopolitical crisis has triggered a broader risk-off environment in financial markets. During periods of heightened geopolitical tension, investors tend to reduce exposure to risk assets and increase allocation to safe havens such as gold, U.S. Treasuries, or major currencies like the U.S. dollar.

For coffee markets, this can mean:

- Widened bid-ask spreads in commodity futures, reducing liquidity for hedgers;

- Heightened short-term volatility, as speculative flows shift away from coffee toward safer assets;

- Risk-adjusted price spikes, where market participants price in potential future disruption even before physical bottlenecks materialize.

Historically, geopolitical shocks elevate the “risk premium” embedded in commodity prices, even when direct supply disruption is limited. For global coffee traders and roasters, this heightens cost uncertainty and hedging expense.

Longer-Term Supply Chain Implications

While the conflict is recent, there are emerging signals of longer-term strategic recalibrations that may impact coffee markets:

- Diversification of routes and multimodal shipping: Importers and logistics planners are likely accelerating investments in alternative corridors and container stocks as a hedge against Gulf-region volatility. This can reduce reliance on any single chokepoint but may raise costs in the near term as redundant capacity is built.

- Production and trade rebalancing: Some importers may accelerate sourcing from producers with more direct access to markets (e.g., Latin America to North America via Panama Canal) to minimize risk exposure.

- Inventory management adjustments: Roasters increasingly hold larger safety stocks in consumer markets — adjusting just-in-time planning to mitigate volatility — which can tie up working capital.

- Insurance and risk management premiums: Insurers may re-price coverage for cargo passing near conflict zones, increasing operational cost for global coffee logistics.

Regional Demand Dynamics

Although Iran and Israel are not global coffee producers, the conflict may reshape regional demand growth. Analysts note that emerging markets, including parts of the Middle East and North Africa, have been expanding coffee consumption faster than mature markets. Growing café cultures and premiumization trends mean that coffee demand elasticity is increasing in regions once considered niche.

Sharp economic downturns or prolonged instability in these markets could temper consumption growth, contributing to demand uncertainty for exporters and roasters dependent on emerging-market revenue.

Conclusion: Complex, Interlinked Pressures

In summary, the Iran–Israel conflict affects the coffee market through multiple indirect — but economically significant — channels:

- Logistics and shipping risk increase costs and delivery uncertainty;

- Energy price inflation raises production and transportation expenses;

- Financial market risk skews investment flows and commodity price volatility;

- Strategic supply-chain adjustments reshape sourcing and inventory practices;

- Regional demand uncertainty may impact medium-term consumption patterns.

None of these forces operate in isolation — together they suggest endurance of higher structural costs in the coffee value chain and a higher baseline for commodity price volatility until geopolitical stability returns. The magnitude of these effects will ultimately depend on how long conflict persists, whether major trade routes are repeatedly disrupted, and how quickly diplomatic de-escalation occurs.

{kind=link}